Who Protects Consumers from the Consumer Financial Protection Bureau?

Washington,

October 24, 2013

Update 11/18/13: The full committee will consider six bills to reform the CFPB on Wednesday.

Next week the Financial Institutions and Consumer Credit Subcommittee will hold a hearing to discuss legislative proposals to bring more accountability, reform and transparency to the Consumer Financial Protection Bureau (CFPB). As Chairman Hensarling has pointed out, the CFPB is arguably the single most powerful and least accountable federal agency in American history. Established by the Dodd-Frank Act, the CFPB's radical design is unique among financial and consumer regulators, including those responsible for consumer and investor protection. Not only does it evade the traditional system of checks and balances championed by James Madison in Federalist #51, it also lacks the internal controls Congress built into other regulatory agencies.

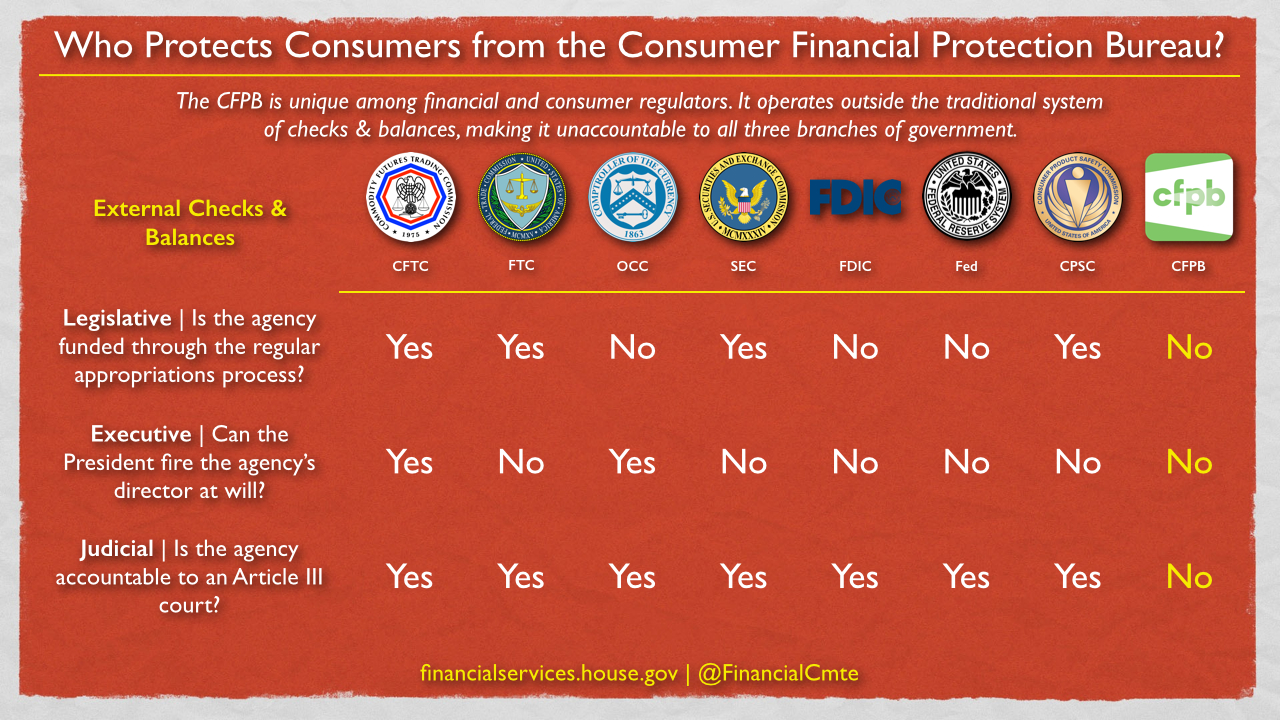

As the chart above illustrates, the CFPB escapes congressional budgetary oversight, obtaining its funding directly from the Federal Reserve instead of through the regular appropriations process. This end-run around Congress leaves no check to ensure the CFPB director is spending the people’s money effectively to promote consumer protection, much less efficiently in this time of runaway debt and deficits. In fact, we've already begun to see the result of this lack of oversight in the CFPB's egregious headquarters renovation costs.

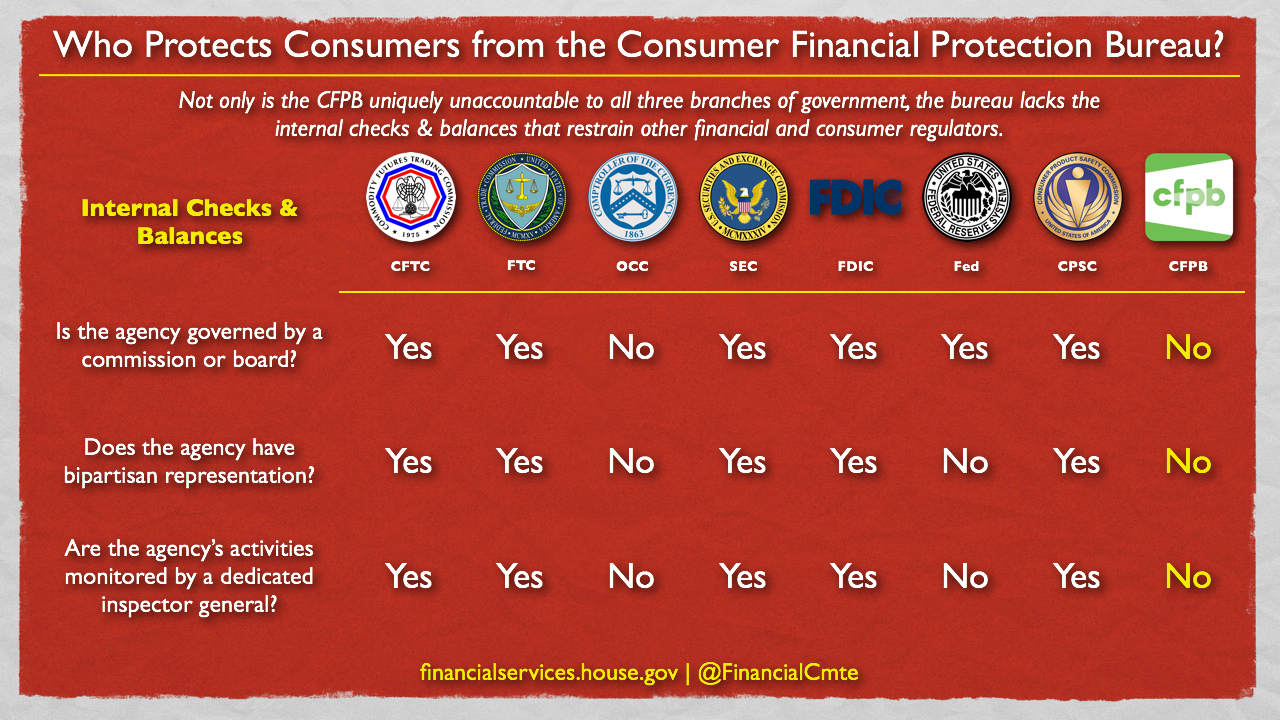

Unaccountable to Congress, we see that the CFPB eludes even the power of the president. The bureau's director, once appointed and confirmed, can only be removed by the nation's chief executive for cause. And don't count on the president to enforce spending discipline or regulatory restraint at the CFPB; the bureau is neither subject to the Office of Management and Budget nor the Office of Information and Regulatory Affairs. The most glaring difference between the CFPB and other regulators in the chart above, however, is the bureau's shocking lack of judicial oversight. Section 1022 of the Dodd-Frank Act provides that where the bureau disagrees with any other agency about the meaning of a provision of a federal consumer financial law, a reviewing court must give deference to the bureau’s view under the Chevron Doctrine. Unfortunately, the absence of external checks and balances is only half the story at the CFPB. As the chart below shows, the CFPB is unaccountable even to itself since there is fundamentally no ‘it,’ no ‘they’ – only a he. Be he our credit czar, national nanny or benevolent financial product dictator, the CFPB director's authority is unilateral, unbridled and unparalleled. Without the check of a bipartisan commission, the director can declare virtually any financial product or service as ‘unfair’ or ‘abusive,’ at which point Americans will be denied that product or service even if they need it, understand it and want it.

Finally, the CFPB lacks a dedicated inspector general (IG) to root out waste, fraud and abuse at the bureau. Given the findings by the Housing and Urban Development IG we highlighted last month, taxpayers should be outraged by this complete lack of accountability, oversight and transparency in the way the CFPB spends the people's money. Defenders of this structure claim it's necessary to guarantee the CFPB's freedom to protect consumers without the influence or interference of politics. Agency independence, however, cannot come at the expense of public accountability. The bottom line is this: consumer protection is not having powerful government agencies 'nudge' consumers to make 'correct' choices in the belief they are incapable of making rational decisions for themselves. True consumer protection empowers consumers and respects their economic freedoms to make informed choices free from government interference and fiat. |